Energy Perspectives

The Unspoken Premise – The Elephant in the Room

Australia’s energy security has always depended on supply more than policy declarations. Despite years of shifting narratives about the role of gas, reality has converged on a straightforward conclusion: the country needs more of it. Domestic production forecasts have pointed to shortfalls in the eastern states and for LNG exports long before net-zero targets became the dominant talking point. The debate has since moved from phasing out gas to managing its scarcity, with reservation policies now proposed as a solution. These policies, however, rest on the assumption, the unspoken premise, that the resource base is fixed and finite. That the gas “pie” cannot be enlarged. It’s the elephant in the room.

That assumption is both limiting and inaccurate. Australia remains significantly underexplored relative to its size. In geological terms, the continent is gas-prone rather than oil-prone. Historical exploration results show that the more wells are drilled, the more gas (and oil) is discovered. Yet the number of exploration wells has fallen sharply over the past two decades, failing to replenish the reserve base that current policy discussions now seek to ration. Without renewed exploration drilling, any gas reservation scheme risks creating only a temporary surplus that will eventually shrink again as supply declines.

The Bamaga Basin offers a direct way forward. Located offshore Queensland in the Gulf of Carpentaria, it sits in an underexplored but geologically promising setting with the capacity to deliver major new gas discoveries. Early assessments indicate the basin could contain sufficient resources to support eastern Australian gas demand for more than 80 years at current consumption levels. Expanding exploration activity in such frontier areas represents the most effective means of growing the gas resource base, restoring balance between supply and demand, and avoiding the price volatility that follows from treating existing reserves as the limit of what is available.

Drilling more wells is the practical response to forecasts of shortfall. Focusing activity in high-potential areas such as the Bamaga Basin can transform the discussion from dividing an existing pie to expanding it.

For more information of the Bamaga Basin click here, and to find out more about the Gulf Energy’s New Frontier Opportunity click here.

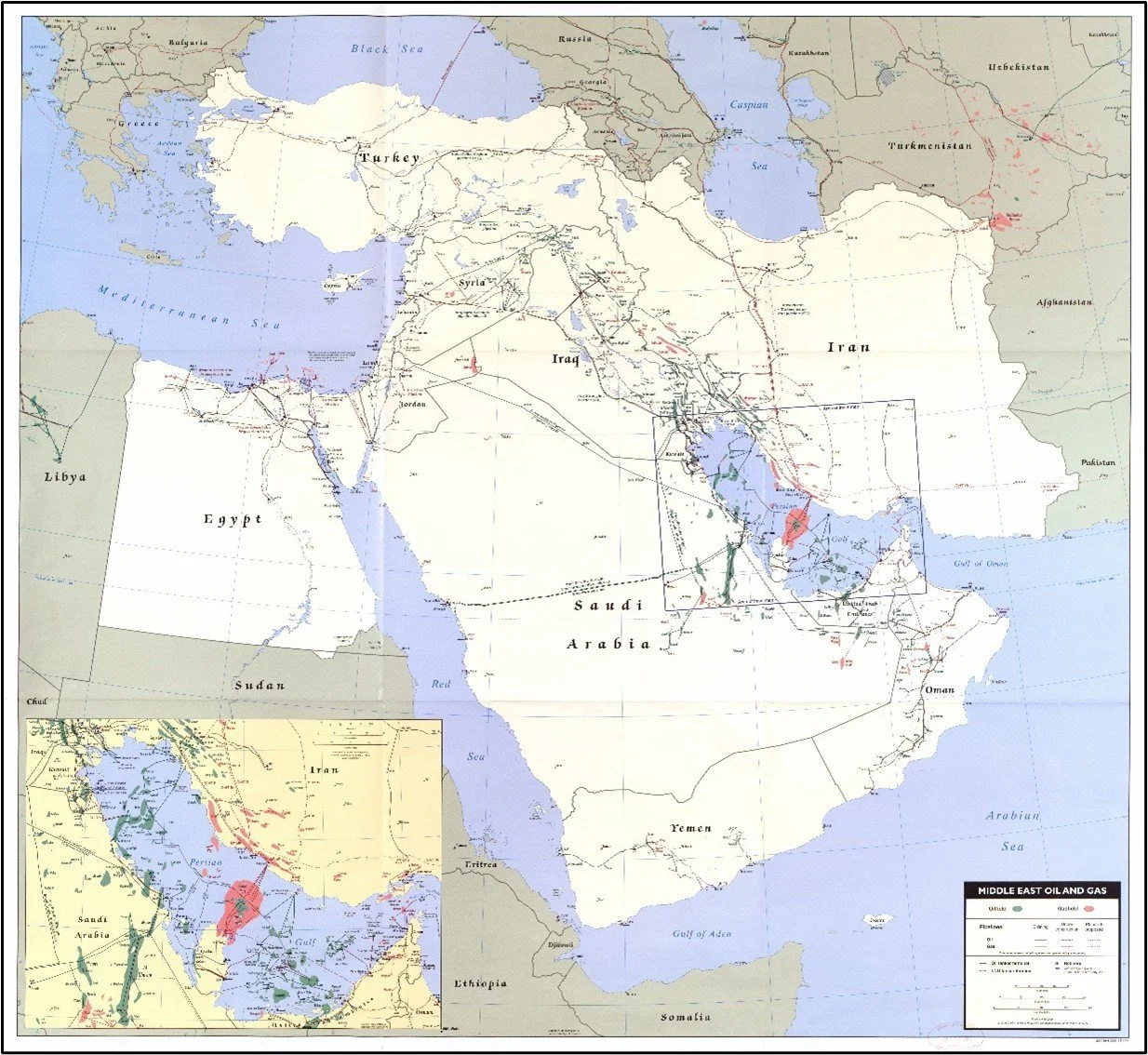

Hope Springs Eternal?

I recently went to a one-day seminar where the theme was the impact of the war in the Middle East on the different parts of the international and Australian oil and gas industry. A common expectation was that it is likely the war will be over in several months’ time and that after a period of settling down and catchup the flow of oil and gas (LNG) would be restored to pre-war levels and prices would decrease. The production and export infrastructure that has been damaged would be repaired, with some facilities, like those related to exporting LNG, may take a few years to be fully re-established. It could be said the atmosphere was cautious but upbeat.

It would seem to me that apparently several important facts were being overlooked, not only at that seminar but by the industry overall. Let me list some of them:

Prior to this war the Strait of Hormuz (SoH) had never been physically blocked. This red line has now been crossed, and a precedent has been set, for all time.

Prior to this war no Middle Eastern country (other than Israel) had attacked the oil, gas and other industrial facilities of its Middle Eastern neighbors. Another red line has been crossed, another precedent has been set, for all time.

Both these precedents have been set by Iran and while currently the violent attacks have come from that country, it is quite possible for other Middle Eastern countries to threaten to or block the SoH in the future. The Strait is withing striking distance of drones and missiles that could be launched in the future from, say Syria, or Iraq or Yemen. The Middle East is volatile, and we have seen several violent regimes and movements in that region in recent times. In fact, it has been reported rebels based in Iraq have attacked Saudi Arabia with drones since the Iran war broke out.

The Middle east is rich in oil and gas, but the options for shipping petroleum around the world, at scale, are geographically constrained. Like the SoH, the Strait of Bab-el-Mandeb (SoBeM), which means "Gate of Grief" or "Gate of Tears", at the southern end of the Red Sea, on the other side of the Arabian Peninsula, could also be easily threatened, as has been demonstrated by the Yemen-based Houthi rebels. Some oil is being piped across Saudi Arabia and loaded on ships which sail through the SoBeM, but the volume is but a fraction that which was being transported by the 130 or so ships that used to travel through the SoH each day, half of which were oil and gas tankers.

Source: Wikimedia Commons

{kind=link}

The Middle East, while endowed with enormous amounts of oil and gas, is geographically constrained, with currently few options to deliver large volumes of petroleum and petroleum products to customers in the event ‘bad actors’ in the region seek to attack facilities of shipping with drones or missiles.

Despite all this, media reports continue to be upbeat and hopeful of a resolution to the conflict, but few have recognised the longer-term challenge the world faces. One of those few is Mr Kevin Gallagher, the CEO of Santos.

An article in the 6 May 2026 edition of the Australian entitled Santos Boss Warns Investors Are Misreading Energy Crisis reported on a recent speech made by Mr Gallagher where he observed that investors appeared too optimistic that current disruptions would be resolved quickly, and predicted there would be a more prolonged period of tight supply and increased risk in global energy markets.

He said, “As traditional supply assumptions are reassessed, buyers are increasingly looking to spread risk across jurisdictions.”.

He went on to say, “What you’ll see is a recognition of supply risk,” Mr Gallagher said. “Customers will look for more diversity in their portfolios.”

I believe Kevin Gallagher is right and, as it becomes more widely apparent, more companies will need to seek sources of oil and gas closer to markets, especially Asia, where transportation routes are less subject to the shipping ‘choke points’ that challenge the Middle East.

Refreshingly Honest, Balanced, and Insightful

These days, the debate about energy and optimal ways to transition is highly partisan, with idealogues dominating the debates and those with alternative views frequently being demonised.

These days the debate about energy and optimal ways to transition is highly partisan, with idealogues dominating the debates and those with alternative views frequently being demonised.

It was therefore noteworthy to me when I came across the transcript of a recent interview titled “Energy guru Daniel Yergin: «I'm sick of the energy transition discussion»”, of Daniel Yergin on the question “Is this the end of the oil age?”. Mr Yergin, often called the most influential energy analyst in the world, is the author of the bestselling Pulitzer Prize winning book “The Prize. The Epic Quest for Oil, Money, and Power” on the history of oil.

The interview is refreshingly honest and balanced, a rarity these days. Rather than me paraphrasing the interview I highly recommend you read it yourself. Let me give you a taste of the realistic tone of Daniel Yergin’s comments by quoting from the beginning of the interview:

Q: Is this the end of the oil age?

“No. Predicting exactly when the demand for oil will fall is like a game. Demand is growing in developing and emerging countries right now. We will probably continue to see growth until sometime into the early 2030s, and even then, demand won’t be dropping precipitously. It will be more of a slow decline.”

Q: So, there won't really be a big sudden change?

“I'm sick of the energy transition discussion. It sometimes loses touch with economic history and reality. If you look at the history of energy transitions, they all last for over a century. To try and make change happen in 25 years, or even half of that time is highly unlikely.”

Q: What is the difference between the current energy transition and previous ones?

“Well, there is one fundamental difference. All of them were energy additions. Oil overtook coal as the world’s number one energy source in the 1960s. But coal hasn’t disappeared. Last year, the world used more coal than ever before, three times as much as in the 1960s. Now we are trying to go from one system to another in a really short time without paying a lot of attention to the amount of resources and minerals that would be required.”

Like I said, Daniel Yergin’s views are insightful, balanced, and framed in realism.

You can read the full interview with Daniel Yergin here found on the nzz.ch website.

More Complex Than We Were Led To Believe

I love it when you get a new insight into something that on the surface looks like it is a booming success with nothing but benefits. For example, the booming installation of solar panels on the rooftops of Australian homes. If you look at this topic narrowly it’s a wonderful success story, but if you investigate more broadly it appears to have created negative flow on consequences for Australia’s energy transition, not readily apparent to the Australian public.

This is revealed by Matthew Warren, former chief executive of the Australian Energy Council, the Energy Supply Association of Australia, and the Clean Energy Council, in his recent piece in the Australian Financial Review entitled “Rooftop solar overload has blown up energy markets”. Here are some excerpts to give you a ‘taste’ of Matthew’s clear, stark, confronting message:

“The biggest hurdle to building a massed renewable engine to power our economy is the growing fleet of renewables already installed. Because they all run at the same time. These headwinds are already materialising relatively early into the renewables adventure.”

“Almost every day 3.4 million rooftops generate more than 10,000 megawatts at their midday peak. This creates chronic oversupply, sending wholesale electricity prices negative…....To manage this growing daily oversupply, every other type of generator that can be curtailed is turned off or dialled back. …..…The biggest hit is on the utility scale wind and solar farms – which are having their

generation increasingly curtailed during the daytime. They earn less and less revenue from the same capital outlay. This pushes up the cost of the electricity they produce and makes new projects less and less profitable. In other words, small-scale renewables are cannibalising the market for large-scale renewables.”

“Rooftop solar PV will deliver around 3 gigawatts of new capacity this year, but large scale is slowing rapidly with constantly eroding value from future electricity output. There are already industry rumours of fire sales of some wind and solar farms.”

“Renewable developers will be buoyed as each coal generator exits, but it will be temporary. Coal cannot exit until enough gas and storage is ready to fill in the big gaps. Gas peakers will keep the lights on, but they won’t fix the renewable oversupply problem. Large-scale storage will soak up surplus electricity, but is proving scarce and expensive.”

“Governments cannot avoid making tough decisions for much longer. Continuing with the status quo will mean each new renewable project will need an increasing injection of cash until governments are underwriting the lot.”

“Shifting electricity demand to the middle of the day would help, particularly passive loads like electric hot water tanks, most of which still heat up at night. More aggressive demand management sounds easy but gets hard because it involves reorganising industries, workforces and daily habits to follow the weather. We can’t even agree on daylight savings.”

“Probably the only way to build massed renewable generation will be as regulated assets, meaning the coup de grace of electricity markets and governments underwriting the whole nine yards. If energy is going to be publicly funded, then how we deliver the transformation should be subject to a lot more critical thinking than it has been to date.”

As Matthew so eloquently concludes, “Whichever way you cut it, energy is going to be more regulated and more expensive, not cheaper. The sooner we stop pretending everything is going OK, the quicker we can address these mounting challenges.”

I strongly encourage you to read Matthew Warren’s whole article here.

Green Energy: Not Cheaper Afterall?

I seem to recall that from the outset, one of the key messages being disbursed by the proponents of the energy transition to non-carbon-based energy sources was that that clean, ‘green’ solar and wind generated electricity would drive down electricity prices for consumers and businesses and be far more economically efficient than coal, gas, and oil. l also remember being sceptical about the enthusiasm with which this message of “cheap electricity” was being broadcast.

It's been a while since then, and recently I have been noticing surprisingly similar comments coming from two enterprises developing solar and wind sourced electricity projects. The Australian Financial Review article (AFR) of 4 November 2023 by James Thomson entitled “Deal drought puts a green question mark over Macquarie” reported Macquarie Group chief executive Shemara Wikramanayake believes governments with massive targets for renewable energy need to realise they will have to pay more to incentivise the necessary investment. Ms Wikramanayake is quoted as saying:

“It’s a big wake-up call for the world. If we want to bring on the supply of renewable energy that we need, we’ve got to step up prices – and we can afford to.’’

A week or so later, in its 15 November 2023 article by Jenny Wiggins entitled “Canadian group highlights the trouble with Australia’s energy ambitions” the AFR reported that the Canadian group OMERS Infrastructure is steering clear of Australia’s planned renewable energy zones, saying the delays in planning and development are pushing up costs and making investments too risky. OMERS claims it’s struggling to close investments in renewable energy projects because of rising interest rates, higher inflation, supply chain disruptions as well as scarce and expensive labour. A senior representative said:

”There are issues with the ‘‘bid-ask spread’’ of what people are willing to pay for energy and what can be delivered in the current market.”

On the same day, another article entitled “The power behind the takeover battle for Origin”, written by Jennifer Hewett, refers to OMERS and its managing director Kevork Sahagian saying it decided to invest in Australia in late 2021 with ‘‘fairly grand ambitions’’. Mr Sahagian said there are significant challenges facing Australia’s energy transition, including higher costs, lack of resources and, importantly, the difference between what energy customers are willing to pay and the price it can be delivered for in this market. He said:

‘‘I think there needs to be some convergence to help facilitate the next wave of investment. I think it is happening, but it’s happening very slowly.’’

It’s likely other players in the ‘green’ energy market are facing similar pressures. At last, the truth is slowly emerging, that ’green’ electricity will not be as cheap as it was portrayed and the increased energy prices resulting from the move to carbon-free electrification are unlikely to be temporary. The real cost of the energy transition is already being felt by Australian consumers who are facing significant difficulties making ends meet in today’s challenges economic environment, and these recent comments suggest high electricity prices in eastern Australia could be a reality for a long time.

The news articles referred to in this commentary can be found via the links below:

1. Deal drought puts a green question mark over Macquarie written by James Thomson for the Australian Financial Review

2. Canadian group highlights the trouble with Australia’s energy ambitions written by Jenny Wiggins for the Australian Financial Review

3. The power behind the takeover battle for Origin written by Jennifer Hewett

Watch Out!

Early in my career a wise mentor advised me to “Watch out you don’t get ‘blind-sided”. It’s a warning from football which describes when you’re so busy watching the action in one direction that you get unexpectedly get tackled from another direction. I’ve learned to always keep this in mind in business.

A recent article in the Australian Financial Review entitled “Swedish sodium-ion battery could minimise reliance on China” (22 November 2023, by Richard Milne) reminded me of this. The news for months has been increasingly reporting the frantic scramble by companies and investors for lithium projects that have the potential to be suppliers of a key component of lithium-ion batteries.

The Northvolt group from Sweden has made a breakthrough in a new battery technology that could minimise reliance on China for the energy transition by developing a sodium-ion battery that has no lithium, cobalt or nickel – critical metals that manufacturers are scrambling to secure, leading to volatility in their prices.

Sodium-ion batteries could be a cheaper, safer alternative to lithium-based batteries because they work better at very high and very low temperatures, but the amount of energy they can produce relative to their size is somewhat less than lithium batteries. Northvolt is working on improving this, with increasing success, and hopes to provide the first sodium-ion battery samples to customers next year and reach full-scale production by the end of the decade.

Lithium is a rare earth element. As the label implies, it’s not easy to find lithium occurring in rocks in high concentrations. When it is found, it’s not easy to refine and process for use in batteries.

In stark contrast, sodium occurs in salt and there’s lots of that in the ocean. It’s not too much of an effort separating sodium from salt either.

There’s a lot of research happening to develop other alternatives to lithium-ion batteries, for example solid-state batteries, hydrogen fuel cells, aqueous magnesium batteries, and graphene batteries. All it will take is for one of these alternatives, which a composed of more commonly available materials, to become commercially viable and lithium batteries will go the way of former rechargeable batteries such as nickel-cadmium (NiCd), and nickel-metal hydrogen (NiMH). Although they dominated only a few decades ago they are now history, blind-sided by lithium-ion.

You can find the articles referred to in this commentary here.

Realistic, and Brave

It all begins with an ideaThese days it’s not often, you find somebody that is prepared to state publicly what they really think,

and to do so in the face of climate and energy debates charged with demonisation of providers of carbon-based sources of energy.

These days it’s not often, you find somebody that is prepared to state publicly what they really think, and to do so in the face of climate and energy debates charged with demonisation of providers of carbon-based sources of energy. The attack comes from an unrealistic, zealous drive to replace traditional energy sources almost instantaneously without acknowledgement of the real cost and time it will take, and the consequences.

In this setting it is refreshing to read the comments of Australia’s Reserve Bank governor Philip Lowe to a Senate estimates committee hearing last Monday, in an article written by Jacob Greber entitled More gas could help lower inflation: Lowe (28/11/2022 Australian Financial Review). The article opens with:

“Reserve Bank governor Philip Lowe has pushed federal and state governments to get more gas into the domestic energy market to curb inflation as federal Labor rushes to finalise a plan that could include a price cap that would potentially discourage investment in new gas wells and pipelines.

Amid calls for redistribution or diversion away from export markets of existing sources of gas, Dr Lowe said the focus should be on what ‘‘we can constructively do to increase’’ supply, which he said would help make a ‘‘substantial contribution’’ to controlling inflation in coming years.”

Lowe is quoted as saying realistically, and bravely:

“One way of tackling inflation induced by supply-side shocks is to address the supply side. And if we can do something on energy and rents next year, inflation will come down quickly.”

Here is somebody prepared to clearly state that the current energy cost crisis (which is contributing to Australia’s inflation) is because there isn’t enough gas supply. The way to increase gas supply, without having to resort to retrospective gas reservation, price caps, excessive taxation and like measures is to simply encourage the search for and development of more gas.

Australia’s geology is known to be gas-prone, and large tracts of the country are either undrilled or sparsely explored. Adapting the time-honoured saying “The harder I work the luckier I get”, the more I drill the more gas I find. It’s as simple as that, but in the superheated current debate about energy and climate, simple, practical truths are not popular.

Jacob Weber’s full article can be found on the Financial Review website here

The ‘Hidden’ Real Challenges of the Energy Transition

Don’t get me wrong, I’m all for a cleaner energy future. The questions in my mind are “What will it cost?”, “What resources are required?”, “How long will it realistically take?” and, importantly, “Do the numbers all stack up?”

Don’t get me wrong, I’m all for a cleaner energy future. The questions in my mind are “What will it cost?”, “What resources are required?”, “How long will it realistically take?” and, importantly, “Do the numbers all stack up?”

I recently reread a refreshingly honest piece, entitled Well-placed to pioneer a clean grid, written by Matthew Warren in the 17 August 2022 issue of the Australian Financial Review, in which he describes the ‘hidden’ real challenges we are facing if the energy source transition Australia is undertaking is to happen smoothly, without massive economic stress and enormous societal dislocation.

The goals set for this task are being driven by aspirations that have disregarded how long the transformation will realistically take and the effort and investment that will be required. As Warren writes in opening his article:

“There are two climate change worlds: the gritty reality of engineering and economics on one side, and the political theatre of ambition and marketing on the other. Function and symbolism. The power and the passion”

The transition is more complex than portrayed, with many interrelated issues. It will involve huge capital investment and long-term changes in peoples’ habits and attitudes. It will cost us a lot and will have a marked impact on our lifestyles. That’s not to say that the transition should not occur. Rather, we need to accept the challenges with a properly informed understanding of what needs to be done and what the realistic costs and time frames are.

I recommend you read Matthew Warren’s full article here.

Brave New World

20th century British philosopher Aldous Huxley, author of the dystopian novel “Brave New World” said: “facts do not cease to exist because they are ignored”.

20th century British philosopher Aldous Huxley, author of the dystopian novel “Brave New World” said: “facts do not cease to exist because they are ignored”.

John Kehoe’s recent Australian Financial Review article, “Rushing the green energy transition will be painful”, plainly lays out the unpleasant facts, and the huge challenges, facing Australia progressing to a carbon-free energy future. He says the writing is on the wall:

“As energy-rich Australia confronts an energy crisis, Germany could be the canary in the coal mine providing a reality check on the great energy transition… The German experience shows that even after huge investments in renewable energy, Europe’s largest economy has nowhere near enough renewable capacity to keep the lights on and businesses alive.”

The unspoken reality is that Germany’s energy decarbonisation process has been facilitated by a lower carbon transition fuel – natural gas from Russia. Once gas was no longer available, they were forced to return to coal and nuclear.

Kehoe clearly lays out the massive, multiple challenges lying before us in Australia, if we are to achieve energy decarbonisation at all, let alone on the time scale set out by our governments. Importantly he urges Australia’s leaders to explain the reality:

“Our political leaders and energy experts must be very frank with the public about the enormity of the task and the financial pain along the way. Without honesty, public support for the energy shift will be lost.”

Kehoe’s article finishes with a caution:

“The events in Germany are a reality check for politicians and activists breezily promoting cleaner, cheaper and more reliable renewable energy”

I urge you to read the full article which can be found online here