Hope Springs Eternal?

I recently went to a one-day seminar where the theme was the impact of the war in the Middle East on the different parts of the international and Australian oil and gas industry. A common expectation was that it is likely the war will be over in several months’ time and that after a period of settling down and catchup the flow of oil and gas (LNG) would be restored to pre-war levels and prices would decrease. The production and export infrastructure that has been damaged would be repaired, with some facilities, like those related to exporting LNG, may take a few years to be fully re-established. It could be said the atmosphere was cautious but upbeat.

It would seem to me that apparently several important facts were being overlooked, not only at that seminar but by the industry overall. Let me list some of them:

Prior to this war the Strait of Hormuz (SoH) had never been physically blocked. This red line has now been crossed, and a precedent has been set, for all time.

Prior to this war no Middle Eastern country (other than Israel) had attacked the oil, gas and other industrial facilities of its Middle Eastern neighbors. Another red line has been crossed, another precedent has been set, for all time.

Both these precedents have been set by Iran and while currently the violent attacks have come from that country, it is quite possible for other Middle Eastern countries to threaten to or block the SoH in the future. The Strait is withing striking distance of drones and missiles that could be launched in the future from, say Syria, or Iraq or Yemen. The Middle East is volatile, and we have seen several violent regimes and movements in that region in recent times. In fact, it has been reported rebels based in Iraq have attacked Saudi Arabia with drones since the Iran war broke out.

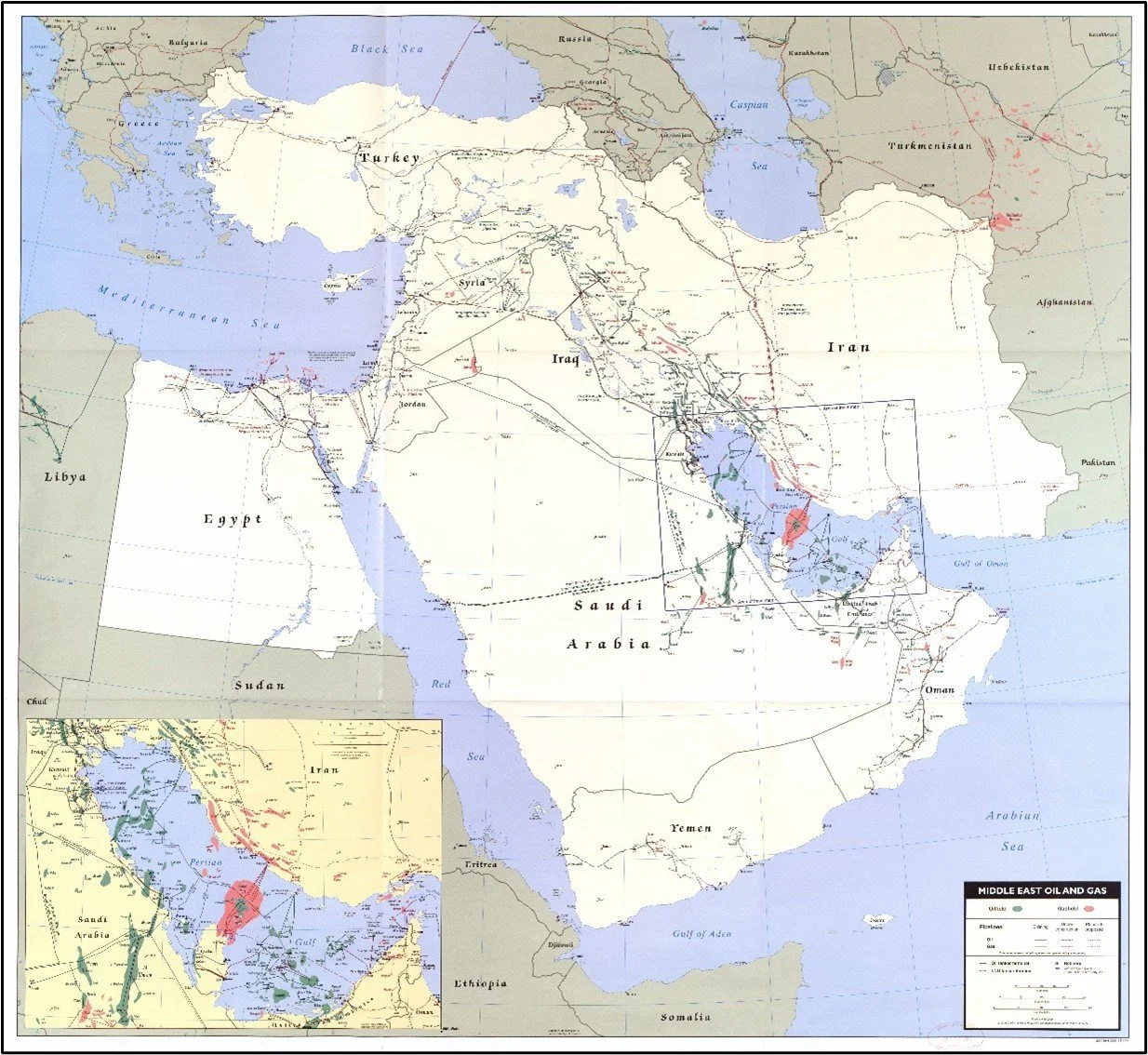

The Middle east is rich in oil and gas, but the options for shipping petroleum around the world, at scale, are geographically constrained. Like the SoH, the Strait of Bab-el-Mandeb (SoBeM), which means "Gate of Grief" or "Gate of Tears", at the southern end of the Red Sea, on the other side of the Arabian Peninsula, could also be easily threatened, as has been demonstrated by the Yemen-based Houthi rebels. Some oil is being piped across Saudi Arabia and loaded on ships which sail through the SoBeM, but the volume is but a fraction that which was being transported by the 130 or so ships that used to travel through the SoH each day, half of which were oil and gas tankers.

Source: Wikimedia Commons

{kind=link}

The Middle East, while endowed with enormous amounts of oil and gas, is geographically constrained, with currently few options to deliver large volumes of petroleum and petroleum products to customers in the event ‘bad actors’ in the region seek to attack facilities of shipping with drones or missiles.

Despite all this, media reports continue to be upbeat and hopeful of a resolution to the conflict, but few have recognised the longer-term challenge the world faces. One of those few is Mr Kevin Gallagher, the CEO of Santos.

An article in the 6 May 2026 edition of the Australian entitled Santos Boss Warns Investors Are Misreading Energy Crisis reported on a recent speech made by Mr Gallagher where he observed that investors appeared too optimistic that current disruptions would be resolved quickly, and predicted there would be a more prolonged period of tight supply and increased risk in global energy markets.

He said, “As traditional supply assumptions are reassessed, buyers are increasingly looking to spread risk across jurisdictions.”.

He went on to say, “What you’ll see is a recognition of supply risk,” Mr Gallagher said. “Customers will look for more diversity in their portfolios.”

I believe Kevin Gallagher is right and, as it becomes more widely apparent, more companies will need to seek sources of oil and gas closer to markets, especially Asia, where transportation routes are less subject to the shipping ‘choke points’ that challenge the Middle East.