The IEA and others forecast, for the foreseeable future, global gas demand will increase

Source: IEA World Energy Outlook 2025

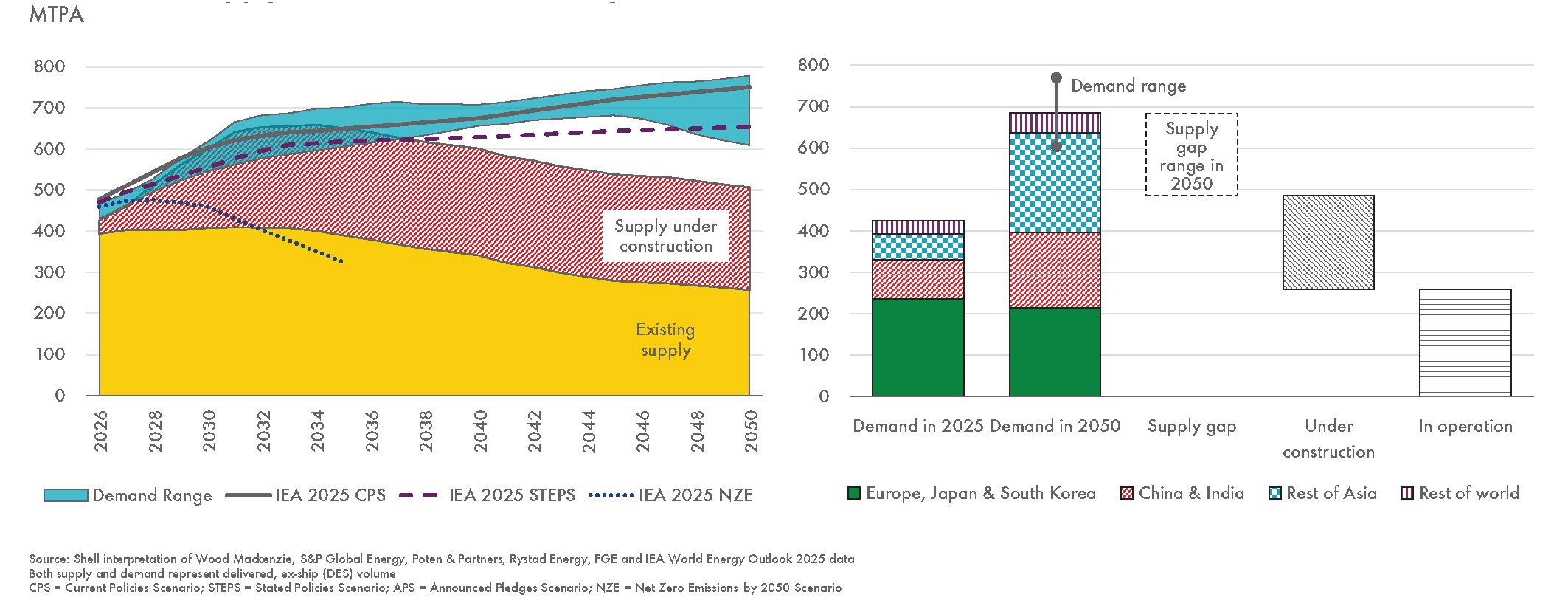

Oil and natural gas supply by scenario to 2050

Source: IEA World Energy Outlook 2025

Much more investment will be needed to meet the growing demand for LNG

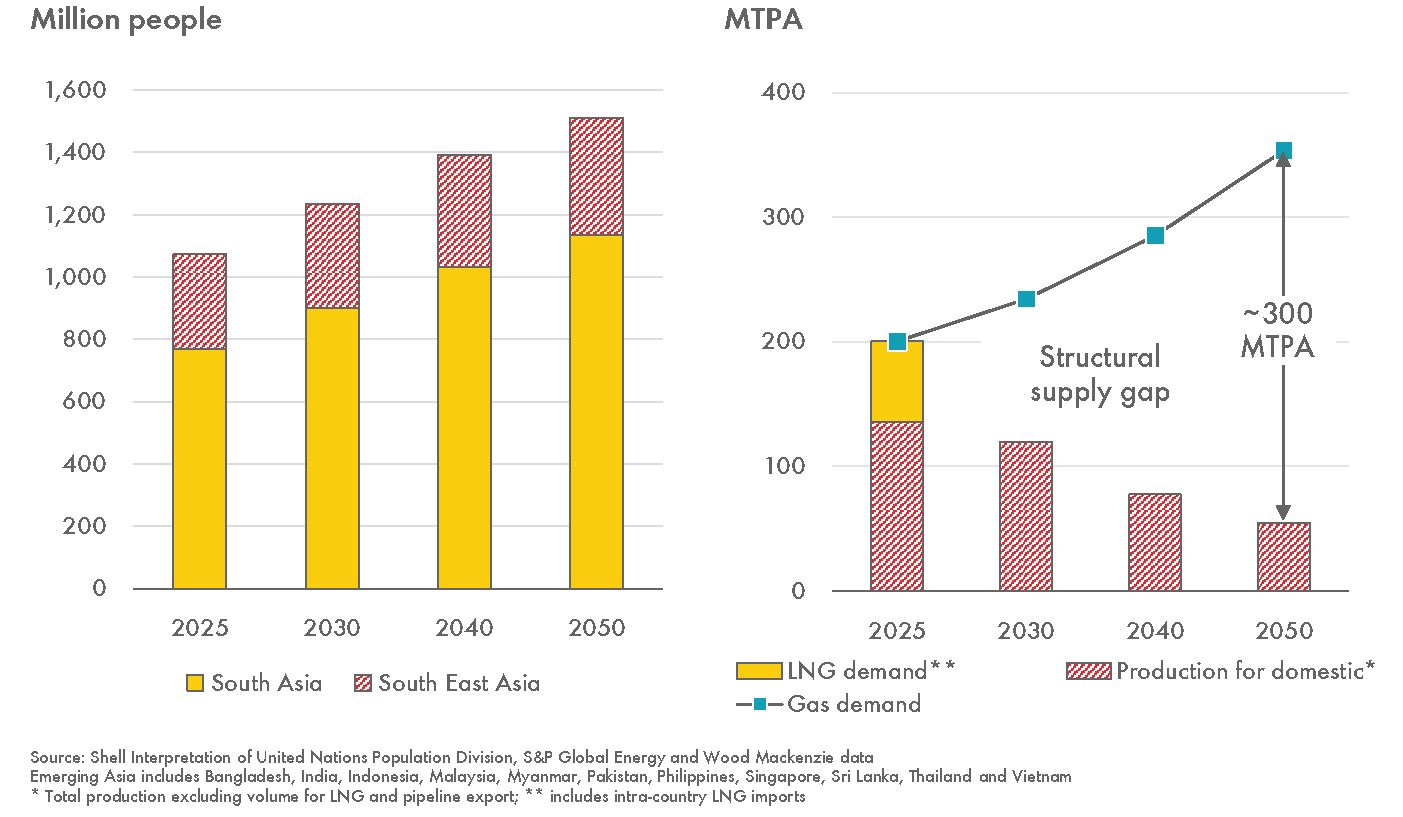

South & SE Asia urban population

Source: Shell LNG Outlook 2026

Source: IEA World Energy Outlook 2025

Output of Australia’s two major competitors (USA & Qatar) has grown, while Australia has contracted

Natural gas is an essential energy globally, but demand is forecast to outpace planned supply

Global LNG supply vs demand forecast range

Source: Shell LNG Outlook 2026

Natural gas is both a transition and a destination fuel. Natural gas and LNG are essential for the energy transition as they play a critical role in shifting away from coal and moving toward net-zero emissions. As the transition evolves, natural gas will remain vital in providing reliable and efficient energy to support economies around the world, including the Asia-Pacific region.

Since the outbreak of the war in the Middle east between The USA and Iran, Asian countries more than most have recognized that they must reduce reliance on any one region or country for energy supplies, including natural gas. The Middle East war has highlighted the need for countries and oil industry companies to secure access to gas, and oil, supplies that are not under threat of attack and which can be transported to customers without having to travel through shipping ‘choke points’, like the Strait of Hormuz.

The re-drawing of global energy supply maps is pushing natural gas and LNG demand to new heights and spurring new opportunities for companies like Gulf Energy.

Emerging Asia gas balance

Natural gas demand increases markedly to 2050, in large part driven by Asia-Pacific power generation and industry

Future major global LNG demand growth will come from emerging and rapidly expanding Asian economies

Global natural gas demand by sector and region in the CPS to 2050

Source: IEA World Energy Outlook 2025

Gulf Energy’s Q/23P Project is ideally located to supply the Asian market

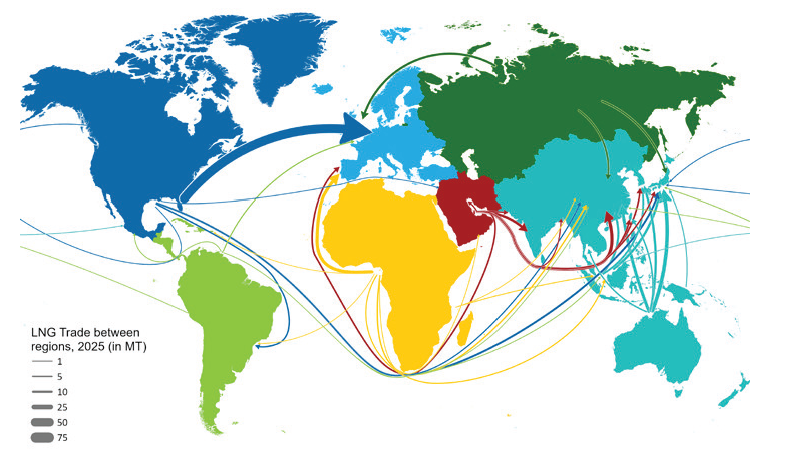

LNG trade between regions for 2025

Source: Rystad Energy

Changes in 2025 LNG exports by market, relative to 2024 (Mt)

2025 LNG market share by exporting country

Australia hasn’t found and developed enough new gas to remain a major global LNG supplier

Australia’s proximity to the rapidly growing emerging economies of Asia gives it a major transportation cost advantage over most of its competitors

Comparative scenarios of global gas demand to 2050

In recent times Australia has failed to maintain a steady stream of new gas production projects being brought online.

Without greatly increased investment in new exploration and upstream infrastructure, Australia will lose its position as a major LNG exporter and will almost certainly lose its energy security.

Source: Rystad Energy